The YTD-26 decline in software-specific public indices1 vs. the relatively flat overall market likely means that the emergence of AI solutions is having a negative effect on all software-as-a-service (“SaaS”) companies. Interestingly, one interpretation of this recent reaction in the public software markets assumes that SaaS companies are capitulating on AI. We do not believe this to be the case. SaaS businesses, whether they have the right to exist or not, and even non-software companies, are investigating how to implement AI in an effort to generate new revenue and reduce the cost of production.

There will be winners among the new crop of native AI companies as well as among the existing SaaS players and there will, of course, be losers in both categories. The outcome for any particular company, SaaS or not, will likely depend on management execution capabilities, flexibility within processes and systems, and an ability to attract talent, specifically to implement these AI solutions.

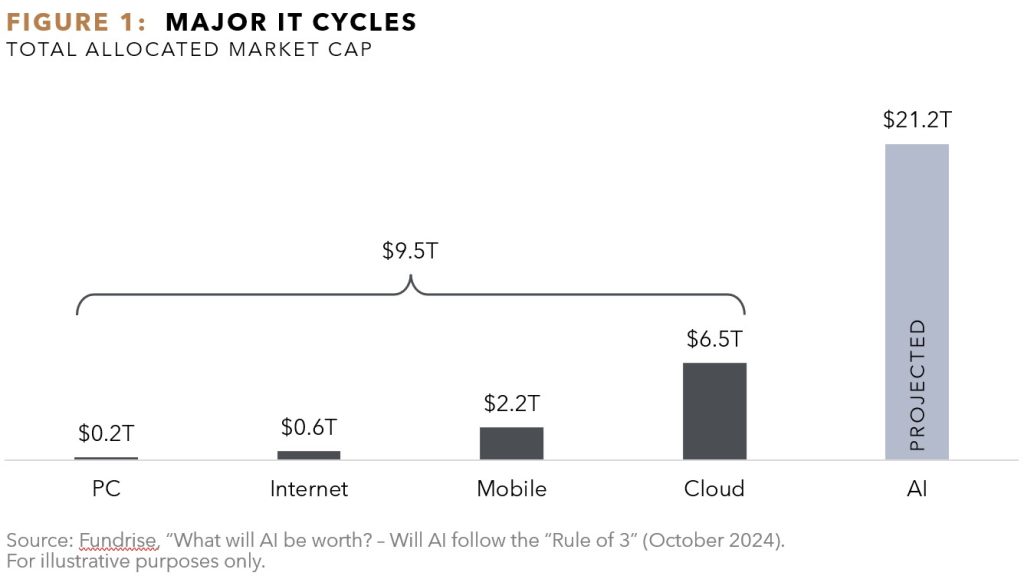

Let us set the context first, however, with a few charts that show the potential impact of AI. Figure 1 suggests that AI-related solutions could be larger than the cloud revolution and perhaps even greater than all of the prior computing innovations combined.

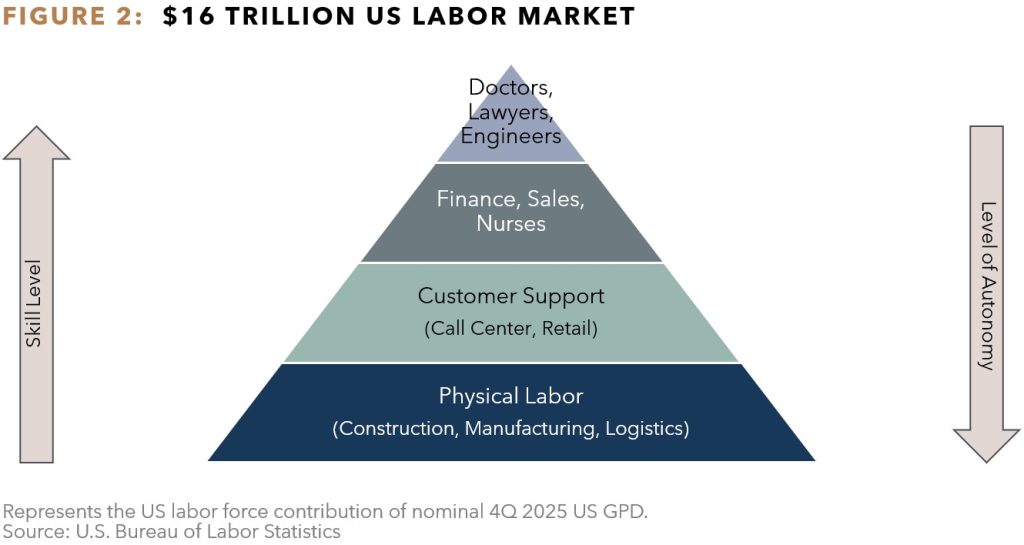

The underlying thesis suggests that AI is likely to affect the entire labor market and potentially displace large swaths of it. For example, let us look at two of the most direct applications of AI: engineering / coding and customer support. AI is often credited with being able to produce basic code within minutes vs. the days or longer it might take a human coder to develop the same code. While an experienced coder could be more productive using AI, an inexperienced coder may be less efficient because they may not know whether, or how, to edit or incorporate the AI generated code. Similarly, customer support is a job which often requires incessant problem-solving skills without becoming burnt out. AI is available around the clock, not emotionally affected by negative customer interactions, and able to handle call routing and scheduling and multiple customers at the same time. Unlike prior technologies that needed to be built from scratch or required infrastructure to deploy, whether it was electricity or the computing network, the delivery mechanism for AI already exists as any user with a phone can download AI and start using the technology.

A SAAS <> AI FRAMEWORK

How will the immense potential of AI solutions affect the current software environment? One way is through an understanding of the three different kinds of existing SaaS companies and how AI is likely to affect the prospects of each. Inspired by the efforts of Alex Rampell, a general partner at Andreessen Horowitz, below is a framework of the SaaS universe:

Well-positioned SaaS businesses:

These businesses provide customers with systems of record that are routinely accessed by software users (constant read / write) and are mission critical to the client’s steady-state functioning. Replacing this software likely imposes high switching costs upon its customers. Importantly, the software / pricing is not affiliated with divisions where seat licenses are based on the number of employees, and therefore, materially unaffected when employees are replaced by AI.

These SaaS players have strong established client bases and provide value-add beyond the software itself, such as professionalized support (distribution, maintenance).

In general, the risk of clients building their own in-house software (e.g., through vibe coding) is minimal due in large part to the complexity and security requirements of the software. Therefore, Tier 1 SaaS businesses are those that offer solutions that cannot be readily displaced by vibe-coded alternatives. Even if ‘vibe coding’ can accomplish ~95% of what a company needs but is unreliable for the remaining ~5%, errors can impose reputational, financial, and legal costs. In addition, Tier 1 players offer a product that can be deployed throughout the enterprise securely and dependably.

The reliability, trustworthiness, and distribution capabilities of these systems of record companies may become even more prized with even higher valuations as Tier 2 and Tier 3 software companies (described below) are disrupted by AI.

An increased investor focus on systems of record companies may very well result in heightened purchase prices for these businesses.

Mixed outlook businesses:

The prognosis for these middle-ground companies relative to the opportunities and threats from AI is currently unclear. One example from history could be the elimination of bookkeepers who drew up physical spreadsheets. Microsoft Excel and other accounting software reduced the number of bookkeepers necessary, but contemporary accountants and FP&A departments may now be more productive than their predecessors as a result and corporate spend on accountancy remains resilient.

In order to mitigate customer losses from AI, these companies will have to create and deepen their own ‘moats’ and make their data and offerings harder to replace.

Another factor that might determine whether a Tier 2 can elevate itself to Tier 1 or become relegated to Tier 3 is how competently AI can adjudicate various “edge cases,” or anomalous situations that the software might encounter. AI might be optimally suited for addressing a majority of situations, but how thoroughly can it learn to adequately confront a situation that was never explicitly enumerated to it?

Poorly positioned businesses:

The public markets may be punishing software businesses whose utility is directly tied to the number of licenses (“seats”) it can sell to its clients. If AI software can complete the work of legions of humans, the customer could very well decide to purchase far fewer “seats” from an oldline SaaS provider. For example, customer service departments may find that they require fewer human employees to route simple calls / tickets due to an AI solution’s proficiency, and subsequently elect to materially cut spend on their legacy SaaS provider.

Alternatively, a vibe-coded solution may also satisfactorily accomplish a client’s needs over a traditional SaaS provider. Tier 3 companies will struggle if their customer’s internal divisions can easily and cheaply build their own solution and make ‘owning’ software cheaper than ‘renting.’

MARGINS

AI native and traditional SaaS companies can reflect fairly distinct margin profiles.

SaaS delivered what was once viewed as the best business model in history.

AI applications presently exhibit a margin profile that is not as profitable as SaaS, and the former can generate muted margins due to high inference costs in some instances.2 In certain respects, a low gross margin posted by an AI start-up could be interpreted as a positive signal indicating that users are truly utilizing the product, which is responding to queries (i.e., the more queries that are run push up inference costs because an AI model has to ‘think’ or compute a response).

Sitting at the top of the software stack, AI applications may be exhibiting muted profitability because they encumber the expense of inference comprised by the cost of GPU chips, electricity, rent from data centers, and the costs of the foundational players through which the queries are run.

These inference costs are expected to decline precipitously as the underlying model technology (and energy / processing requirements) continues to improve representing a “Moore’s Law” for AI.2

Even if inference costs do not decline rapidly, AI businesses could still generate profits through higher revenue as their products continue to expand and gain traction through the replacement of Tier 2 / 3 software companies as observed above. However, those companies may not be valued at the levels that investors are expecting today should lower margins hold.

VALUATIONS AND PUBLIC MARKET REACTIONS

The valuation of public markets, particularly public software companies, could be considered to be priced to perfection, as public holdings are theoretically reflective of all information available to every market participant. Announcements that growth at SaaS businesses may not surpass expectations have resulted in sometimes acute corrections.3

The market may be throwing the baby out with the bathwater. We believe some SaaS companies will continue to not only exist but thrive with their own AI implementations. The challenge is to figure out which will prevail (i.e., Tier 1 companies) and which may fail (Tier 3 companies).

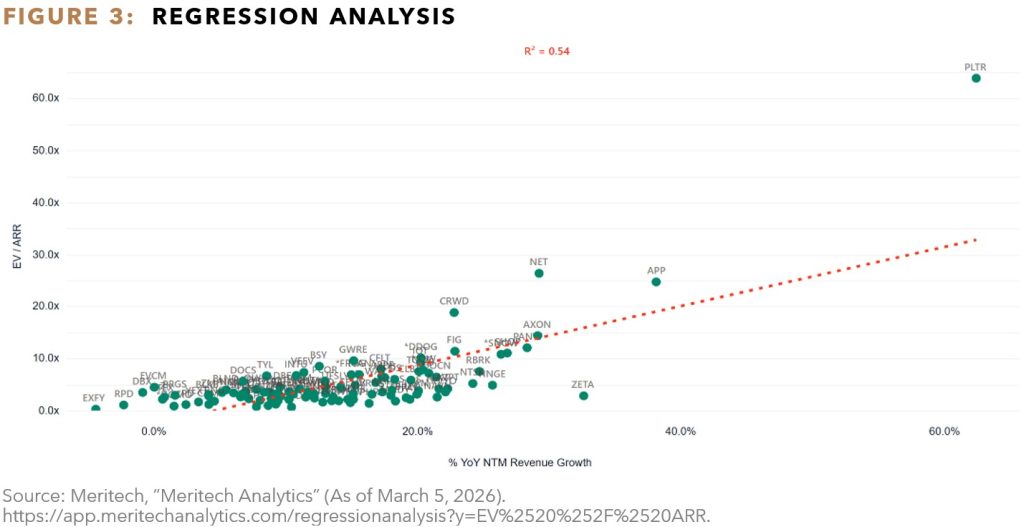

As detailed in Figure 3, some of the more established public market SaaS companies are growing between 15-20% with the fastest growing 60%. However, AI companies are presently expanding at a faster clip than their SaaS counterparts, having notched triple-digit year-over-year revenue gains since 2023.4 Even though the valuations of public software companies may decline, there is a financial rationale to pricing private AI assets at higher multiples.

Customer CTOs may continue maintaining their existing SaaS products, but could be withholding approval for new projects and saving budgets for AI-related solutions. It would not be surprising if while SaaS-based revenue of a private company is flat, its new AI products are generating hundreds of millions of sales within a short period of time.

However, despite seemingly robust growth in revenue exhibited by certain AI-native startups or products, investors must determine whether that revenue is sticky, and what valuation those revenues are worth. That valuation question has fundamentally been the challenge for any new market development. Getting in at the right price with a transformative technology can lead to substantial returns. Paying too much, however, even with the correct thesis, may lead to mediocre results if not outright losses. This is a crucial and difficult factor to consider in the AI market today.

A FUTURE OF DISRUPTION

While it is not obvious how or which companies will be changed by AI, it seems inevitable that AI will have a profound impact on companies, technologies, and the humans that inhabit this planet Earth. Will AI enhance the productivity of workers or be one of the few technologies that actually destroys labor (with potential gains accruing to the asset owners)? Could any systemic productivity gains from AI temper inflation and warrant lower interest rates?

Perhaps most importantly for the markets, what valuations should investors ascribe to both existing SaaS and emerging AI businesses as the technological shift evolves? Successful (and perhaps lucky) investors will select the companies that are able to capitalize upon AI’s trends while avoiding those that are wiped out by it.

FOOTNOTES AND IMPORTANT INFORMATION

1YTD-26 as of March 9, 2026. BVP Nasdaq Emerging Cloud Index: https://cloudindex.bvp.com/; S&P Software & Services Select Industry Index: https://www.spglobal.com/spdji/en/indices/equity/sp-software-services-select-industry-index/#overview

2A16z, State of the Markets (as of January 22, 2026): https://a16z.com/state-of-markets/

3Meritech, Time’s Up for Saas (Grow Faster of Vanish) (as of February 5, 2026): https://meritech.substack.com/p/times-up-for-saas-grow-faster-or; Financial Times, Salesforce chief dismisses ‘SaaS-pocalypse’ fears of AI overtaking business software (as of February 25, 2026): https://www.ft.com/content/b74b8227-d7cb-4976-ba95-a3a27b79cbdd

4A16z, State of the Markets (as of January 22, 2026): https://a16z.com/state-of-markets/

IMPORTANT INFORMATION

This information is presented solely for informational purposes and should not be viewed as a current or past recommendation or an offer to sell or the solicitation to buy securities or adopt any investment strategy. Offerings are made only pursuant to a private offering memorandum containing important information. The opinions expressed herein represent the current, good faith views of the author(s) at the time of publication. There is no assurance that any events or projections will occur, and outcomes may be significantly different than the opinions shown here. This information, including any projections concerning financial market performance, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Past performance is not a guide to future results and is not indicative of expected realized returns.

The views and information provided are as of March 2026 unless otherwise indicated and are subject to frequent change, update, revision, verification and amendment, materially or otherwise, without notice, as market or other conditions change. There can be no assurance that terms and trends described herein will continue or that forecasts are accurate. Certain statements contained herein are statements of future expectations or forward-looking statements that are based on Abbott’s views and assumptions as of the date hereof and involve known and unknown risks and uncertainties (including those discussed below and in Abbott’s Form ADV Part 2A, available on the SEC’s website at www.adviserinfo.sec.gov) that could cause actual results, performance or events to differ materially and adversely from what has been expressed or implied in such statements. Forward-looking statements may be identified by context or words such as “may, will, should, expects, plans, intends, anticipates, believes, estimates, predicts, potential or continue” and other similar expressions. Neither Abbott, its affiliates, nor any of Abbott’s or its affiliates’ respective advisers, members, directors, officers, partners, agents, representatives or employees or any other person is under any obligation to update or keep current the information contained in this document.

This material is for informational purposes only and is not an offer or a solicitation to subscribe to any fund and does not constitute investment, legal, regulatory, business, tax, financial, accounting or other advice or a recommendation regarding any securities of Abbott, of any fund or vehicle managed by Abbott, or of any other issuer of securities. No representation or warranty, express or implied, is given as to the accuracy, fairness, correctness or completeness of third-party sourced data or opinions contained herein and no liability (in negligence or otherwise) is accepted by Abbott for any loss howsoever arising, directly or indirectly, from any use of this document or its contents, or otherwise arising in connection with the provision of such third-party data.